Wasde Report December 2025 (Commentary)

Please Note: This text was summarized using generative AI. Readers should verify all details against the original source document.

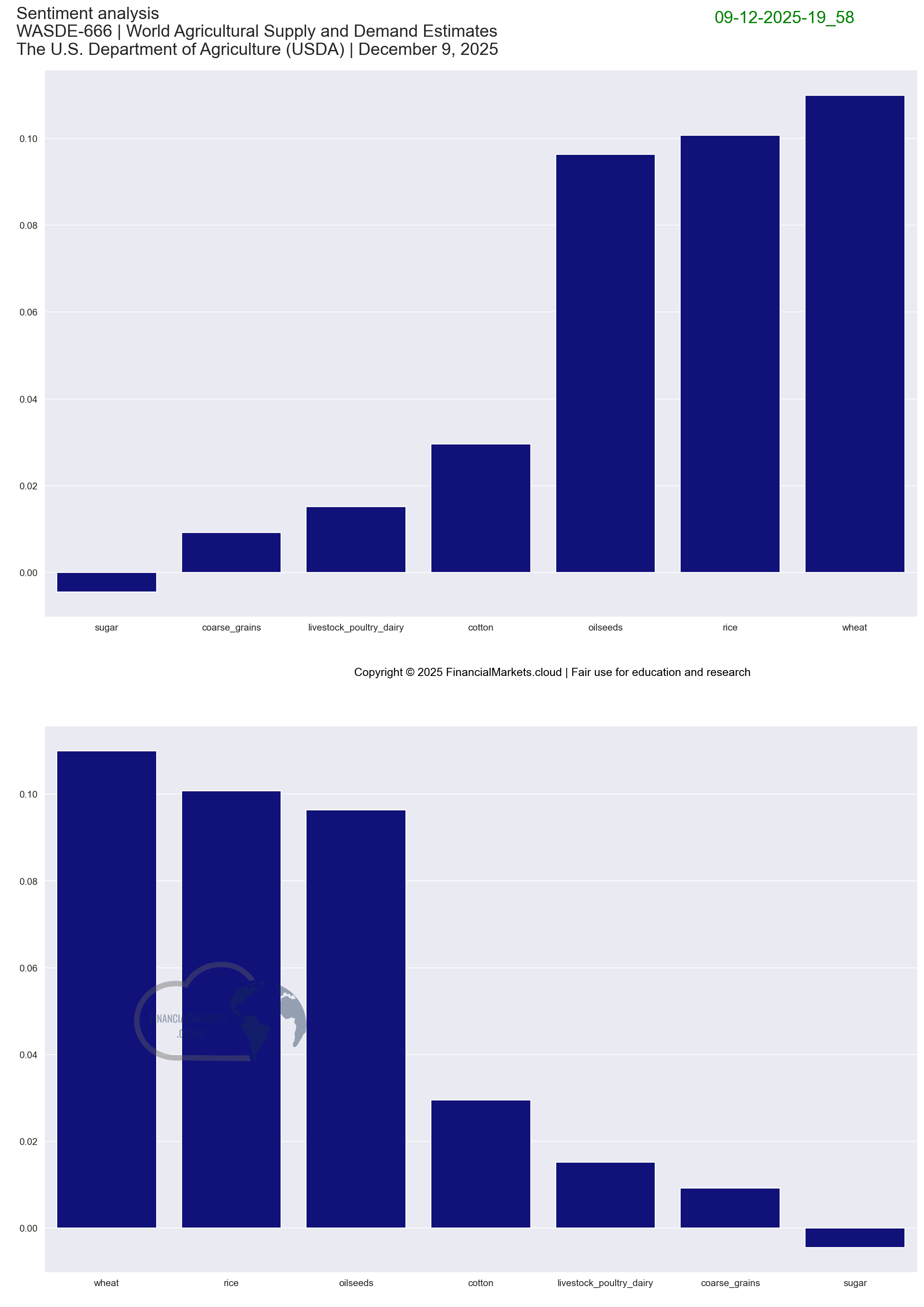

Wheat

December’s report maintained consistent U.S. supply, use, and farm price for wheat. However, shifts occurred within individual categories, particularly in by-class revisions for feed and residual use, and exports. The global wheat forecast remained bullish with increases across supplies and consumption. Major contributions to supply surges came from record output in Canada and Argentina, with the EU also recording significant growth. Expanded exports were noted from Australia and Canada, while global ending stocks rose to 274.9 million tons showing the first year-to-year increase since 2019/20, primarily driven by boosts in output from key exporters.

Coarse grains

U.S. corn exports continued to expand, with shipments expected to exceed 800 million bushels for the September-November quarter. Despite stable domestic supply, rising exports reduced ending stocks to 2.0 billion bushels. The season-average farm price maintained at $4.00 per bushel. On a global scale, production slightly declined, led by downturns in Ukraine and Canada, although positive adjustments were noted for the EU where Poland was among countries with increased yield predictions. Despite increased exports, global corn stocks showed a reduction to 279.2 million tons, reflecting broader trade dynamics and production challenges.

Rice

The outlook for U.S. rice showed decreased supplies due primarily to a reduction in imports, coupled with reduced exports, particularly to Latin America. Ending stocks rose as domestic use remained unchanged. The season-average farm price was significantly lowered by $1.10 per cwt. Globally, supplies increased mainly due to higher beginning stocks in India. Although world production decreased, global trade forecast went up slightly, and ending stocks increased to 188.8 million tons, driven largely by India’s increased stock levels.

Oilseeds

Soybean scenario remains steady with unchanged supply, use, and pricing forecasts. Globally, oilseeds production is expected to increase due to rises in rapeseed, peanuts, and soybeans, despite some decreases in sunflower seed production. Specifically, rapeseed production showed a significant rise, especially in Canada. World-ending stocks for soybeans see a moderate increase, primarily driven by higher stocks in Brazil and Russia, despite reduced exports from Ukraine and Benin. On a global scale, crush utilization grows slightly on enhanced supplies from Russia and India, while imports shift with reductions in several countries but an increase for Brazil.

Sugar

The U.S. sugar supply for 2025/26 shows minor adjustments from November, with a slight decrease in imports counterbalanced by higher production in Louisiana and Florida. Beet sugar production saw a decrease due to higher beet pile shrink forecasts. Sugar deliveries for human consumption show minor decreases amid ongoing demand weakness and industry uncertainties expected for 2025/26. Ending stocks reached 1.867 million STRV, reflecting a stocks-to-use ratio of 15.2%. In Mexico, despite unfavorable weather reducing sugarcane yields, production projections increased slightly, with exports projected at 800,000 MT including licensed shipments to the U.S.

Livestock, poultry, and dairy

December 2025 saw a mixed outlook in the meat markets with higher beef and poultry but lower pork production due to slaughter data. Broiler production increased, while turkey production was affected by HPAI culling. Imports and exports predictions are adjusted, reflecting recent trade and tariff changes. The beef export forecast was reduced beyond 2026 while pork exports are expected to increase. Dairy forecasts for 2025 show strong demand, keeping butter exports competitive, although cheese prices declined. Overall, the forecast for 2025 and 2026 reflects fluctuating demand and recent price data, with a mixed outlook contingent on international trade conditions and domestic supply challenges.

Cotton

The U.S. cotton production forecast increased slightly to 14.3 million bales due to higher yields, while mill use decreased significantly, reaching the lowest level in nearly 150 years at 1.6 million bales. Consequently, ending stocks are projected at 4.5 million bales, representing 32.6 percent of disappearance. The farm price is projected to fall to 60 cents per pound. Globally, there are small reductions in production, consumption, and trade, but ending stocks increased slightly. The global stocks-to-use ratio remains at a steady 64 percent.

Text sentiment analysis